Meta Description: UAD 3.6 is changing residential appraisal reporting forever. Discover the complete compliance checklist appraisers need before the November 2026 deadline, including dynamic URAR updates, software readiness, QC changes, and AMC expectations. Go Source Valuation Blog

The Industry Is Moving Faster Than Most Appraisers Realize

For y

With the rollout of UAD 3.6 and the redesigned dynamic URAR, Fannie Mae and Freddie Mac are replacing the traditional static appraisal structure with a data-driven reporting model that changes how appraisal information is captured, validated, reviewed, and delivered.

The mandatory adoption date is November 2, 2026. After that point, new GSE appraisal submissions using legacy UAD 2.6 formats will no longer be accepted.

For appraisers, this is not simply a software update. It is a workflow transformation that affects reporting logic, quality control, review expectations, and lender compliance standards.

Read More: Go Source Valuation Blog

What Makes UAD 3.6 Different?

The most visible change is the replacement of multiple legacy appraisal forms with one flexible, dynamic URAR structure.

Under the old system, appraisers selected different forms depending on property type:

- 1004 for single-family homes

- 1073 for condos

- 1025 for multi-family properties

- 2055 for exterior-only assignments

Under UAD 3.6, those separate forms are consolidated into a single adaptable report structure that changes based on assignment characteristics and property data.

But the larger shift is happening behind the scenes.

Instead of relying heavily on narrative commentary, UAD 3.6 emphasizes structured, machine-readable appraisal data. Quality ratings, condition adjustments, property characteristics, and market data now flow through standardized fields designed for automated analysis and faster lender review workflows.

This modernization supports automated collateral review systems, AI-powered QC tools, and more scalable appraisal processing across the mortgage industry.

Why Appraisers Need to Prepare Early

Many appraisers assume the transition can wait until 2026. That assumption creates risk.

The optional use period already allows lenders and AMCs to begin processing UAD 3.6 for appraisal submissions. Early adopters are actively testing workflows, training review teams, and updating systems before mandatory adoption arrives.

Appraisers who delay preparation may face:

- Increased revision requests

- Submission delays

- Compatibility issues with AMC portals

- Lower appraiser scorecard performance

- Reduced lender preference

Meanwhile, appraisers who adapt early are likely to become preferred partners for AMCs seeking reliable UAD 3.6-ready professionals.

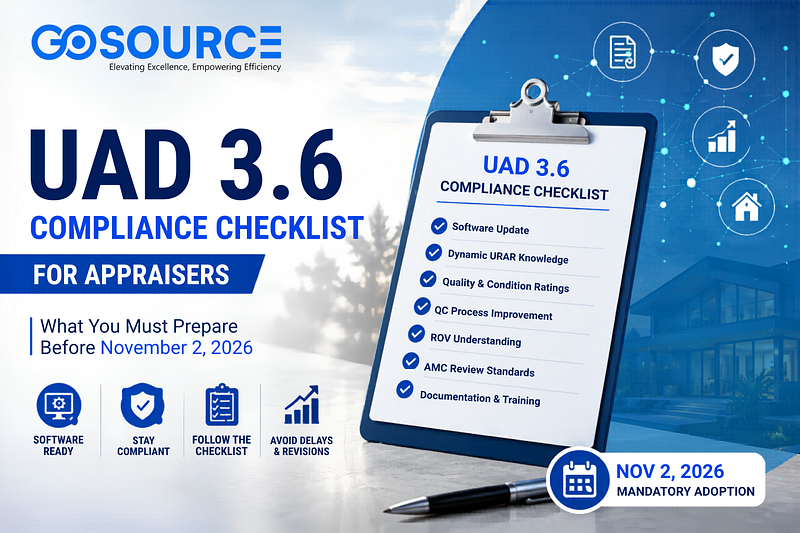

Complete UAD 3.6 Compliance Checklist for Appraisers

1. Confirm Your Software Vendor Is UAD 3.6 Ready

Your appraisal software platform is the foundation of your transition.

Contact your software provider immediately and confirm:

- UAD 3.6 support timeline

- Dynamic URAR compatibility

- XML schema support

- UCDP submission readiness

- Testing availability during the optional use period

Do not assume your software is automatically compliant. Written confirmation matters.

2. Learn the Dynamic URAR Structure

The new URAR format changes how appraisal data is organized and presented.

Appraisers should study:

- Dynamic sections

- Scenario-based reporting logic

- Structured data fields

- Updated property characteristics

- Revised market analysis sections

Fannie Mae and Freddie Mac have already released sample URAR documentation and training materials designed to help appraisers prepare for the transition.

3. Update Your Quality and Condition Rating Knowledge

UAD 3.6 introduces clarified definitions for quality and condition ratings to improve consistency across appraisal reports.

This means appraisers must become more precise when documenting:

- Deferred maintenance

- Renovation quality

- Functional utility

- Construction characteristics

- Property updates

The new standards reduce ambiguity, but they also reduce flexibility for vague reporting language.

4. Improve Your Appraisal Quality Control Process

UAD 3.6 creates a much more data-sensitive review environment.

Modern appraisal QC now focuses heavily on:

- Structured data accuracy

- Comparable consistency

- Adjustment logic

- Compliance alignment

- Automated validation checks

AMCs and lenders are strengthening QC workflows to reduce revision cycles and underwriting delays.

Appraisers should build internal pre-submission review routines before sending reports to clients.

5. Understand the New ROV Expectations

The updated UAD framework introduces a more standardized Reconsideration of Value (ROV) process aligned with federal fair lending expectations.

Appraisers should prepare for:

- More structured reconsideration requests

- Increased documentation expectations

- Greater review transparency

- Enhanced audit trails

Clear support for adjustments and comparable selection will become even more important in moving forward.

6. Train for Faster AMC Review Standards

Appraisal review teams are already updating their workflows to align with UAD 3.6 structures.

That means reviewers will increasingly focus on:

- Data consistency

- Structured field accuracy

- Missing required information

- Compliance gaps

- Narrative alignment with structured data

Appraisers who submit cleaner reports with fewer inconsistencies will likely see faster approvals and stronger AMC relationships.

The Appraisers Who Adapt Early Will Win More Orders

Industry transitions always create separation between early adopters and late adopters.

Appraisers who begin preparing now can position themselves as:

- Reliable UAD 3.6-ready professionals

- Low-revision appraisers

- Faster-turnaround partners

- Compliance-focused vendors

- Preferred AMC panel members

As AMCs and lenders evaluate vendor readiness throughout 2026, appraisers who already understand the new reporting structure will stand out immediately.

How Go Source Valuation Supports UAD 3.6 Readiness

At Go Source Valuation, we are actively preparing appraisers, lenders, and AMCs for the UAD 3.6 transition through operational support, appraisal review services, quality control workflows, and appraisal management solutions aligned with the new reporting standards.

Our teams are already working with evolving appraisal workflows designed for the dynamic URAR environment, helping clients reduce revisions, improve compliance, and prepare for the November 2026 deadline.

For more industry insights, visit the Go Source Knowledge Hub.

Frequently Asked Questions

What is UAD 3.6?

UAD 3.6 is the updated Uniform Appraisal Dataset, introduced by Fannie Mae and Freddie Mac, to modernize residential appraisal reporting with a new dynamic URAR format.

When does UAD 3.6 become mandatory?

Mandatory adoption begins on November 2, 2026, while legacy UAD 2.6 will be retired in May 2027.

What is the dynamic URAR?

The dynamic Uniform Residential Appraisal Report replaces multiple static appraisal forms with one adaptable report structure that changes based on assignment type and property characteristics.

Why is UAD 3.6 important for appraisers?

UAD 3.6 changes how appraisal data is structured, reviewed, and validated. Appraisers who prepare early will reduce revision risk and improve lender and AMC compatibility.